{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Key takeaways

This year, PwC’s 11th Global Consumer Insights Survey queried urban consumers on their purchasing studies before, and after, the COVID-19 outbreak. With billions of people concentrated in the world’s cities, 80 percent of the world’s GDP emanates from their economic activity.1 The behaviour of these cutting-edge consumers is of interest in understanding consumption patterns before and after the pandemic, and their implications for businesses.

What we found is that for companies that cater to the end-consumer, the future is arriving more quickly than imagined, with the COVID-19 pandemic accelerating digital trends that had already been transforming consumer behaviour.

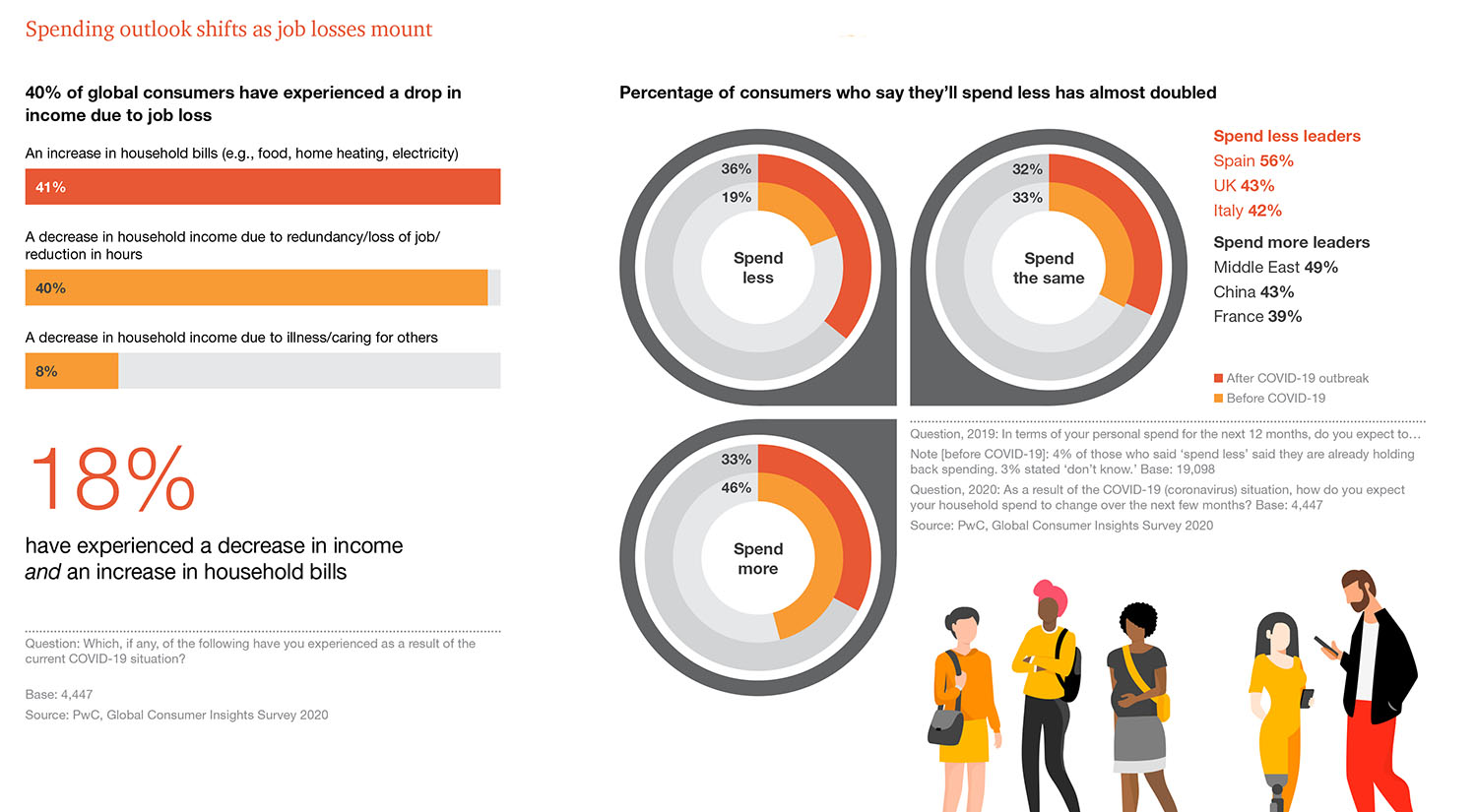

The bottom line is that with goods and services, businesses need to expect market volatility and price sensitivity in the coming months. Understandably, COVID-19 has deeply affected urban consumers’ views on spending — before the outbreak, consumer confidence was high, with almost half (46 percent) of survey respondents saying they expected to spend more in the next 12 months.

In subsequent interviews, however, 40 percent reported a decrease in income as a result of job loss or redundancy. In addition, the percentage of those who said they were going to spend less in the next few months almost doubled and the number who said they were going to spend more dropped by more than 10 percentage points.

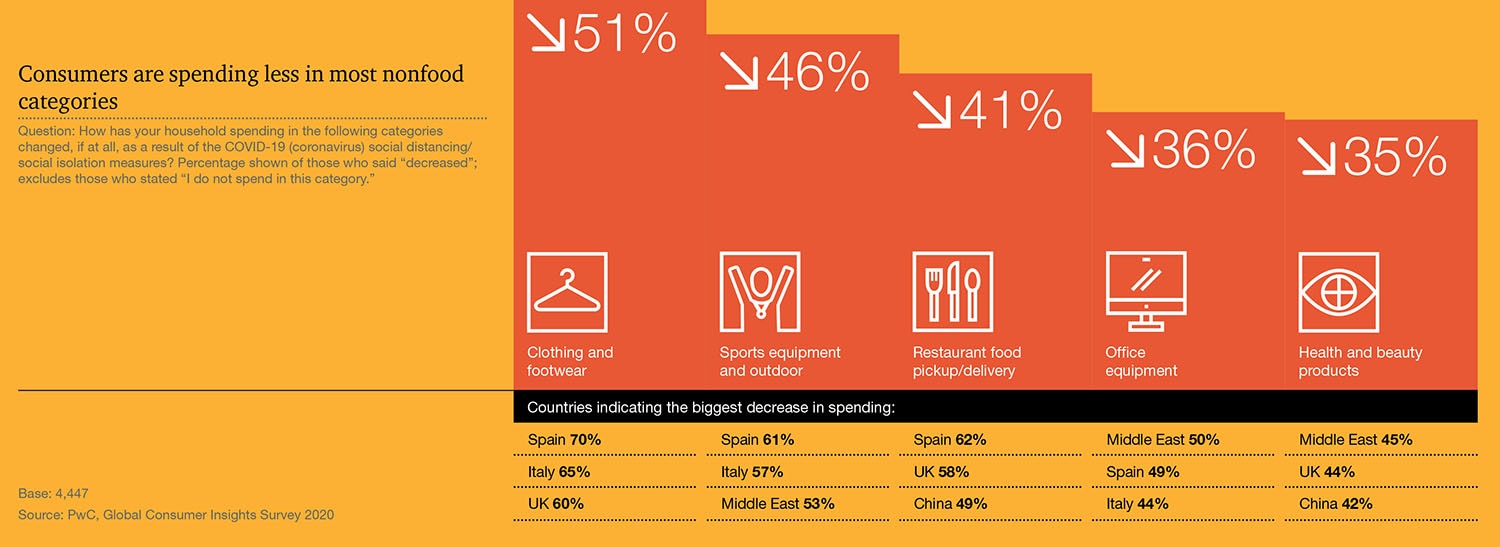

Before isolation measures were put in place, urban consumers were opening their wallets for travel, dining out, art and cultural events, personal styling, health and wellness, nightlife and entertainment, and sporting events. Travel and dining out were two of the top three ways city dwellers spent disposable income, with 44 percent and 41 percent of respondents choosing those categories, respectively.

Since the outbreak, people are now spending the most on groceries, in-place entertainment and home projects. They’re also making fewer food shopping trips but filling up bigger baskets. Most nonfood items are bought online and, with the exception of entertainment and media, consumers are spending significantly less.

While in store purchases require their own special approach (namely, giving consumers solid assurance that places of business have a plan to make their customer experience as safe as possible), online, there has been a significant shift that also requires attention.

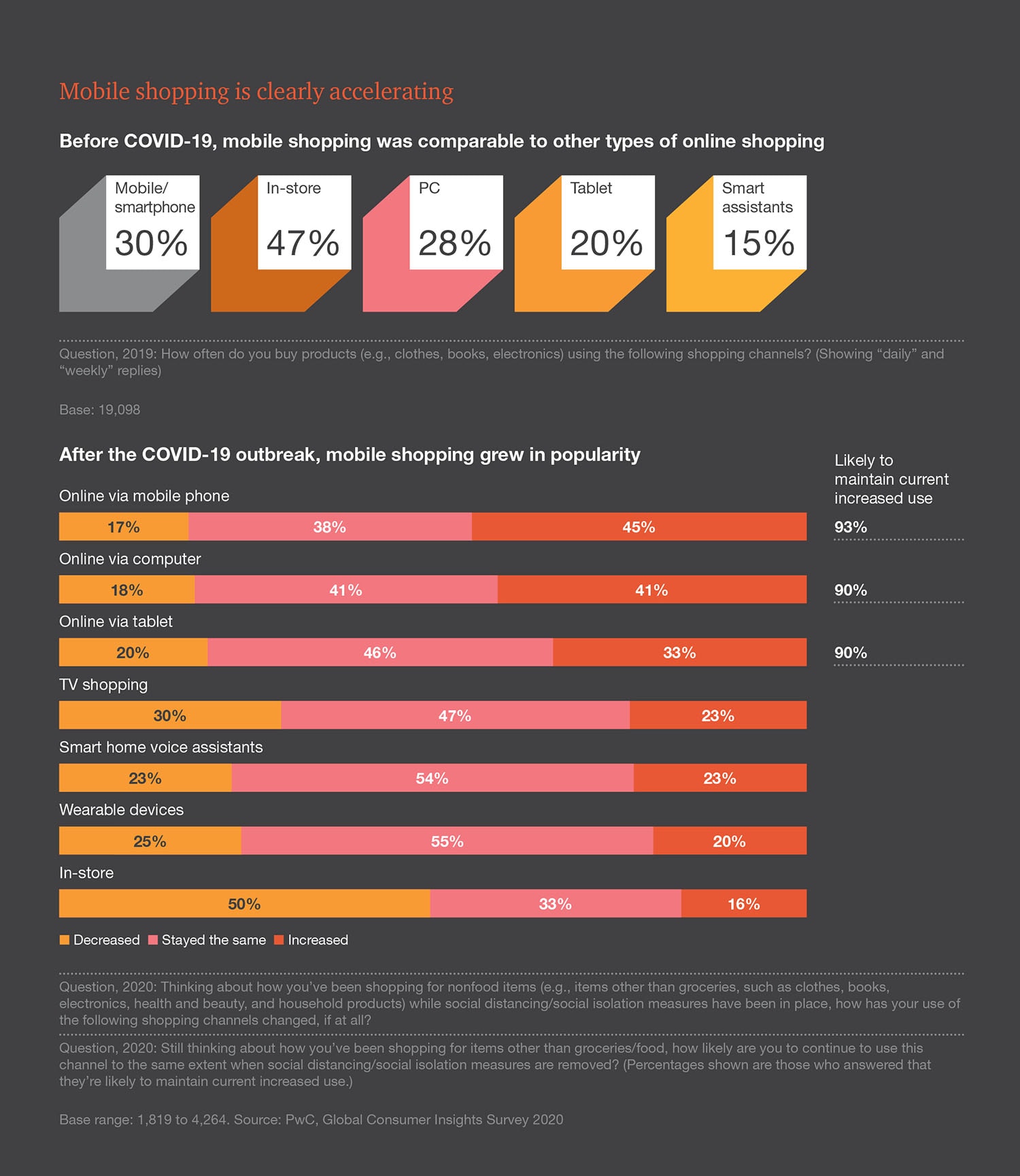

The pandemic has reinforced the already growing trend of online shopping, as well as encouraging experimentation. Consumers are exploring different ways to access products and services and accelerating certain behaviours that have long been simmering in the background.

When we first surveyed urban consumers in late 2019, mobile online shopping was becoming more popular, and since the outbreak, our research again shows that a significant percentage of consumers say they’ve increased their mobile shopping. This trend is especially pronounced in China and the Middle East, with 60 percent and 58 percent of respondents, respectively, saying they’ve started shopping more on their mobile phones. And most respondents said they’re likely to maintain their current increased use after isolation measures are lifted.

Mobile shopping isn’t the only digital trend the pandemic has jump-started. Before the outbreak, online grocery shopping was well behind online shopping for nonfood items. But what was unfathomable to many just a few months ago — buying fresh produce online, for example — has become the new normal in many countries.

The belief among some data professionals and consumers before the pandemic was that urban broadband networks were fragile and underdeveloped. But in fact consumers we talked to have been satisfied overall with their broadband speed during their time in isolation — 69 percent globally say they’re satisfied or extremely satisfied with the speed of broadband in their home.

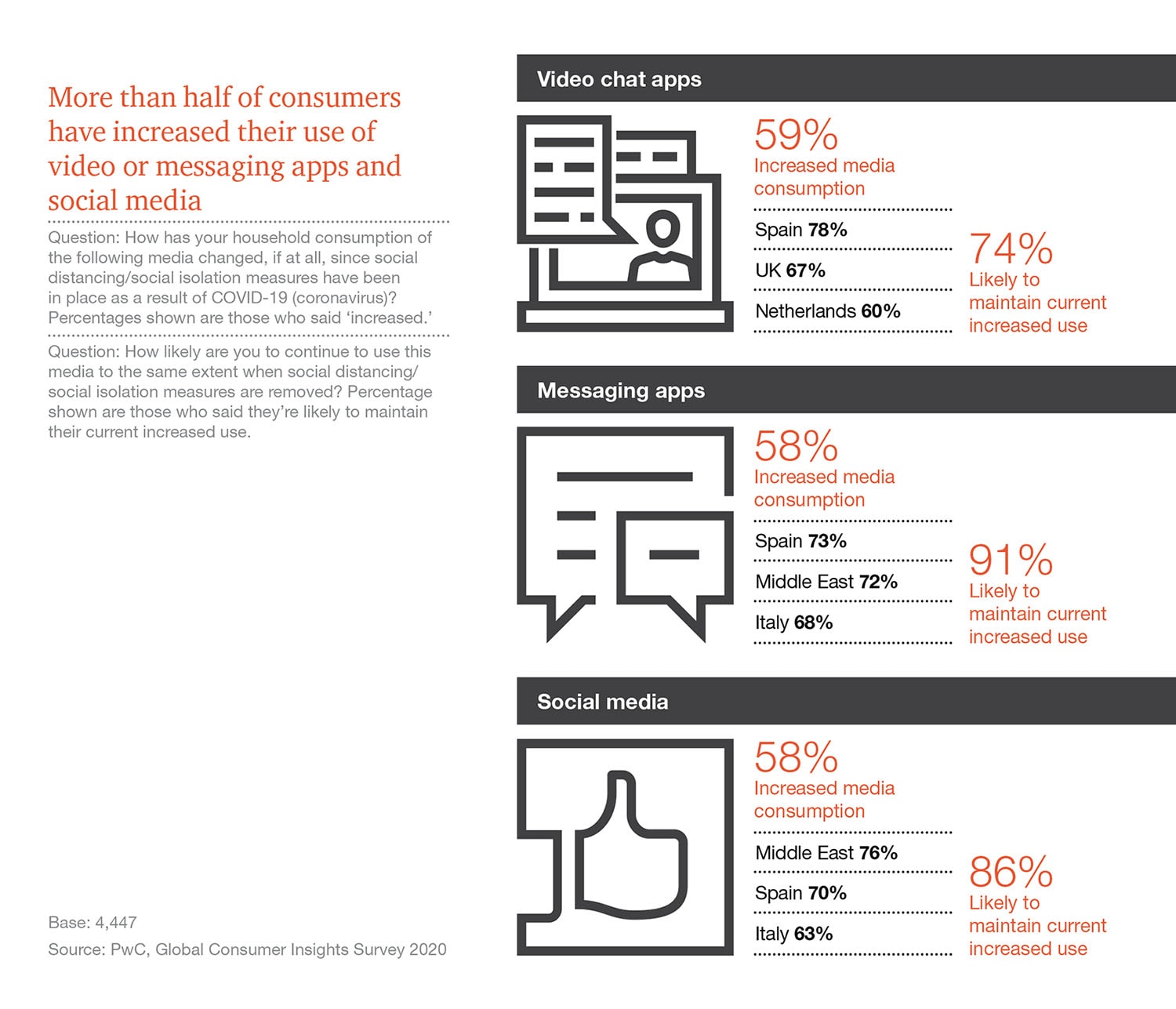

And it’s not just networks that are ready for the digital revolution. People are now equipped with and well-versed in a broad array of digital tools for virtual work, communications and socialising. Since we started surveying consumers 11 years ago, we’ve found more consumers each year adopt social media platforms and apps to enable communication or shopping, yet the increases have largely been incremental and it was unclear if they would continue to use the apps.

The pandemic, however, has accelerated adoption. Most notably, the majority of these adopters say they’ll continue to use video chat apps, messaging apps and social media more than they used to even after isolation measures are eased.

COVID-19 shutdowns have greased the digital runway, and as some new virtual habits become ingrained, the shift to a more digital world for those who can afford its tools and experiences will become even more pronounced. This evolution will further polarise customer segments into those who have digital resources or aptitude and those who don’t.

While businesses shouldn’t write off physical stores — 49 percent of global urban consumers say non-food in-store shopping has stayed the same or increased during the pandemic — COVID-19 has clearly highlighted the benefits of mobile shopping — its ease, portability and immediacy. Consumer insights suggest mobile commerce will retain this momentum and likely accelerate, particularly as it has made leaps and bounds in grocery. But the overarching trend will be toward an omnichannel experience, with consumer-facing companies needing to seamlessly integrate their offline and online experiences.

Given the significant uptick of online grocery during stay-home measures, the resilience of physical grocery visits, and the time it will take for consumers to feel confident returning to dining in restaurants, grocery should be a very strong sector over the next year.

We’ll also most likely see retailers offer a greater spectrum of click-and-collect services as consumers limit their exposure and reduce trips. Global trends such as curbside pickup and delivery services in grocery, general merchandise and electronics have grown in popularity, and will be here to stay. Mobile shopping will also be expected to fill the vacuum created by physical shopping that doesn’t bounce back due to bankruptcies and closures.

The trend of more consumers embracing online also bodes well for 5G networks. Companies will be able shore up their capabilities, increase adoption and bring the online experience to life for a captive cohort. We’ve already seen the introduction of virtual selling platforms that help showcase products, engage consumers, and provide much richer service levels than say a chat box. Such platforms will proliferate across categories.

As tools such as digital sizing in fashion, virtual shoppers, consumer collaboration platforms and augmented reality are introduced and begin to converge, companies should:

The pace of change and industry disruption under way will likely continue to drive the emergence and establishment of a new cohort of winners and laggards over the next decade, with the consumer at the centre like never before. For business, the need to understand how this new, increasingly digital, world affects touch points with customers will be crucial to actively reinventing their future.

For further insights into what consumers are looking for in this new normal, and the experiences and products needed to keep them, download the full Global Consumer Insights Survey.

Donna Watt

Partner, PwC Australia

References