{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

As climate change challenges intensify, global investors are grappling with how to fund solutions and companies that address emissions reduction and climate resilience. PwC’s latest State of Climate Tech report, released last month, reveals key differences between global and Australian investing behavior. It sheds light on shifting behaviors, emerging opportunities and untapped potential. Among the key findings, Australian investors stand out for their resilience but also for gaps in areas like AI-driven innovations. In this article, we explore these trends, the differences between global and Australian markets, and the opportunities for Australian investors to create greater value through 2025.

Report scope:

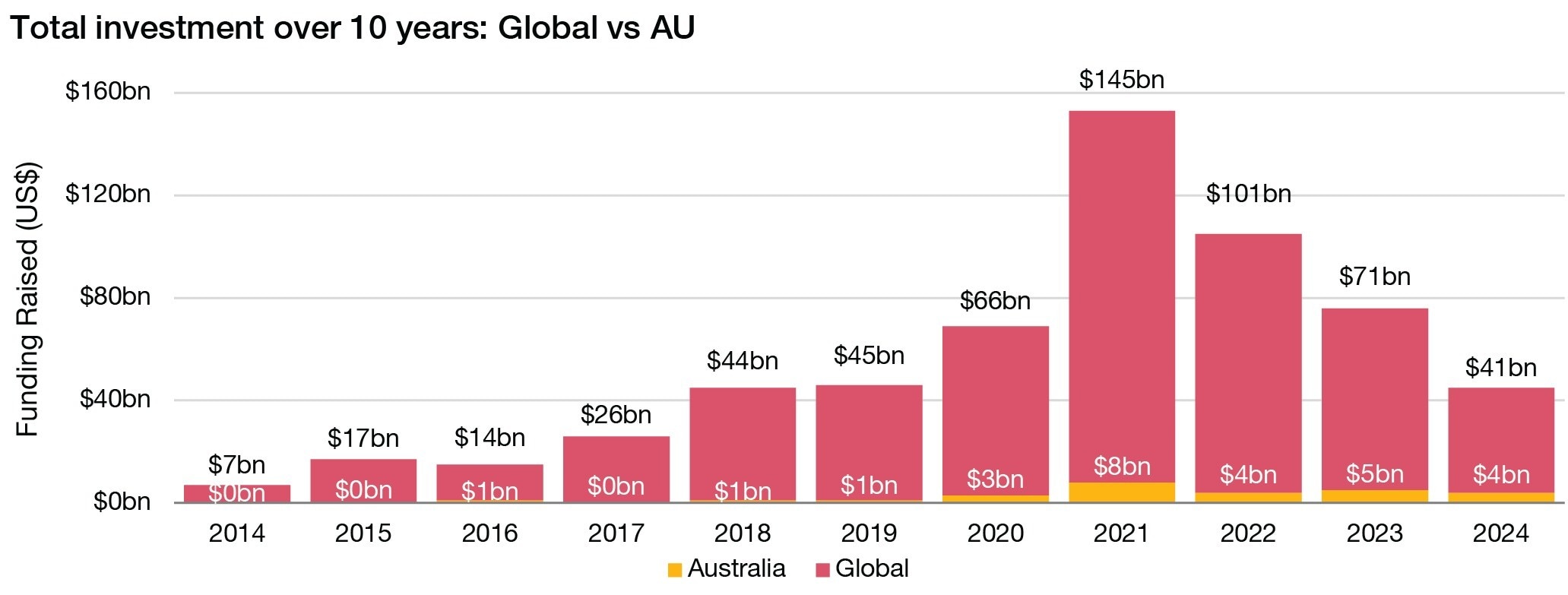

Global: 52,000+ deals; US$600bn+ of investment

Australia: 1000+ deals, US$27bn+ of investment

Over the past year, as higher borrowing costs and uncertain economic conditions weighed on the broader deal-making market, climate tech investment has declined. Globally, climate tech financing dropped 29%, bringing it below pre-2019 levels. In Australia, however, investment remained more resilient, with only a 12% decline in the same period and staying above 2020 levels, reflecting a stronger local market.

In fact, 2024 investment into climate tech startups from Australian investors is $237m more than it was in 2022, compared to the global slump which has seen a $60bn decline in investment worldwide. Given the number of deals has declined, this could reflect a strategic shift by Australian investors toward fewer, larger deals to de-risk with a real focus on returns.

For several years, AI has been a busy segment of the venture investing market — and investors’ enthusiasm for AI has carried over into climate tech. Globally, AI-related climate tech investment has surged, growing from $5bn in 2023 to $6bn in the first three quarters of 2024. It accounted for 14.6% of total global climate tech funding. The key funding segments are autonomous vehicles (62% of AI-related investment) and industrial applications across agriculture, smart homes and smart energy solutions (20%).

In contrast, in Australia investment in AI-related climate tech dropped sharply, from $700m in 2022 to $100m in the first three quarters of 2024, with limited diversification (mainly focused on industrial applications). This could be due to economic uncertainty, market saturation after the initial excitement around AI, concerns around ROI and startups moving overseas to get traction in more lucrative markets.

AI is uniquely positioned to accelerate the climate tech transition by scaling innovation and driving profound systemic change.1 Australian investors are missing opportunities to promote innovation and enhance long-term competitiveness.

Corporations that operate outside the financial sector make up a vital part of the climate tech ecosystem. They purchase and use climate technologies. They license technologies or acquire start-ups to tap into the growth opportunities associated with demand for climate solutions. And they provide financing to climate tech start-ups, investing through their own balance sheets and through corporate venture capital (CVC) units.

Globally, over the past few years, large, non-finance companies have taken part in around a quarter of climate tech deals: 28% of deals in the first three quarters of 2024.

In Australia, corporate participation was significantly higher, at 46%, with joint deals almost doubling since 2019. Australian corporations are also focused more on mid- and late-stage investments (74% of deals compared to 61% globally). Although, this upward trend towards the later stages of the investment life cycle is consistent with global findings — this year’s figure is more than twice that of 2018 (and considerably higher than the 33% share among finance-sector investors in 2024). This shift may reflect companies’ growing interest in scaling up proven climate technologies rather than placing bets on technologies that are less developed.

Australian corporations are playing a crucial role in scaling climate tech solutions, outpacing global trends. This highlights their pivotal role in driving the sector forward.

Diversify your portfolio: Leverage underfunded segments like AI in Australian climate tech, where there is less competition and significant growth potential.

Expand Corporate Venture Capital (CVC): Use CVC to support early-stage startups for early access to innovative solutions or focus on scaling proven technologies through late-stage investments that align with corporate sustainability goals.

Focus on high-emission sectors: Invest in sustainable solutions tailored to Australian core industries or climate challenges, that have the opportunity to be scaled globally.

If you would like to find out how we can help with your climate ambitions, please contact Jon Chadwick.

Funding for climate tech start-ups is down. But PwC’s global climate tech analysis shows that patient investors are still finding opportunities.

PwC Australia

General enquiries, PwC Australia

{{item.text}}

{{item.text}}