Share this article

This article outlines a number of current ideas about the state of the carbon market and the pathways it's on. It also discusses some of the emerging opportunities in this rapidly growing marketplace. It is written for carbon emitters, creators of carbon credits and other participants in the Carbon Market – ultimately the marketplace needs to accommodate both sides of the carbon equation to function and deliver the energy transition outcomes we all need.

The value of carbon

When discussing the value of carbon, we often start with this conundrum: ‘How do you place a value on not doing something that you can’t measure (at least directly)?’

Recent announcements, such as the Chubb Review and the proposed Safeguard Mechanism reforms, indicate continuing progress to address the decarbonisation challenge. This progress together with international growth and increasing liquidity are all indicators that the carbon markets are maturing and that we are likely to end up with a globally connected marketplace filled with opportunities to generate economic benefit.

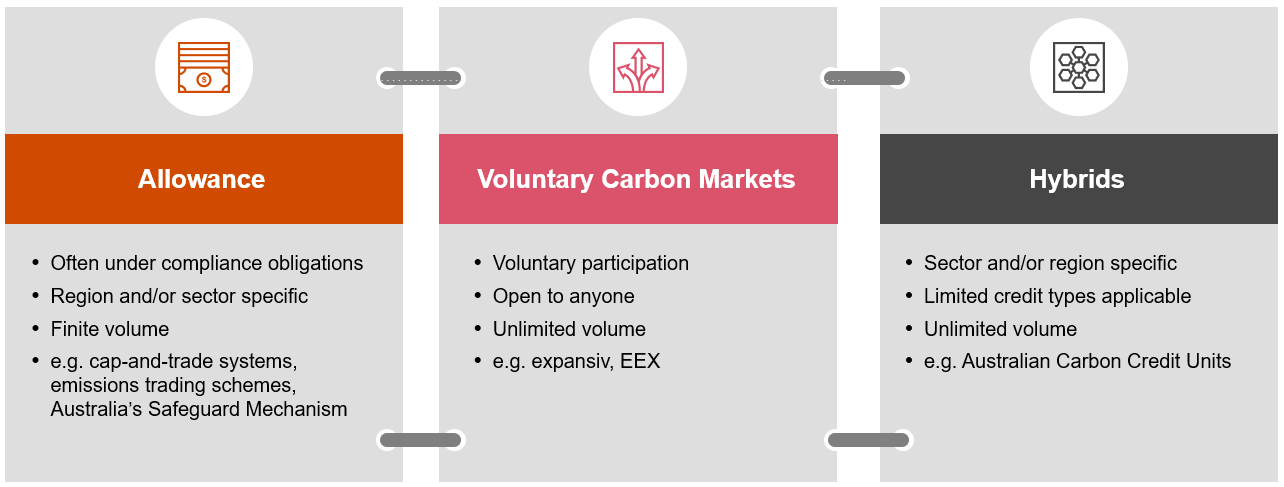

Types of carbon markets

There are three main types of carbon markets: allowance, voluntary and hybrid.

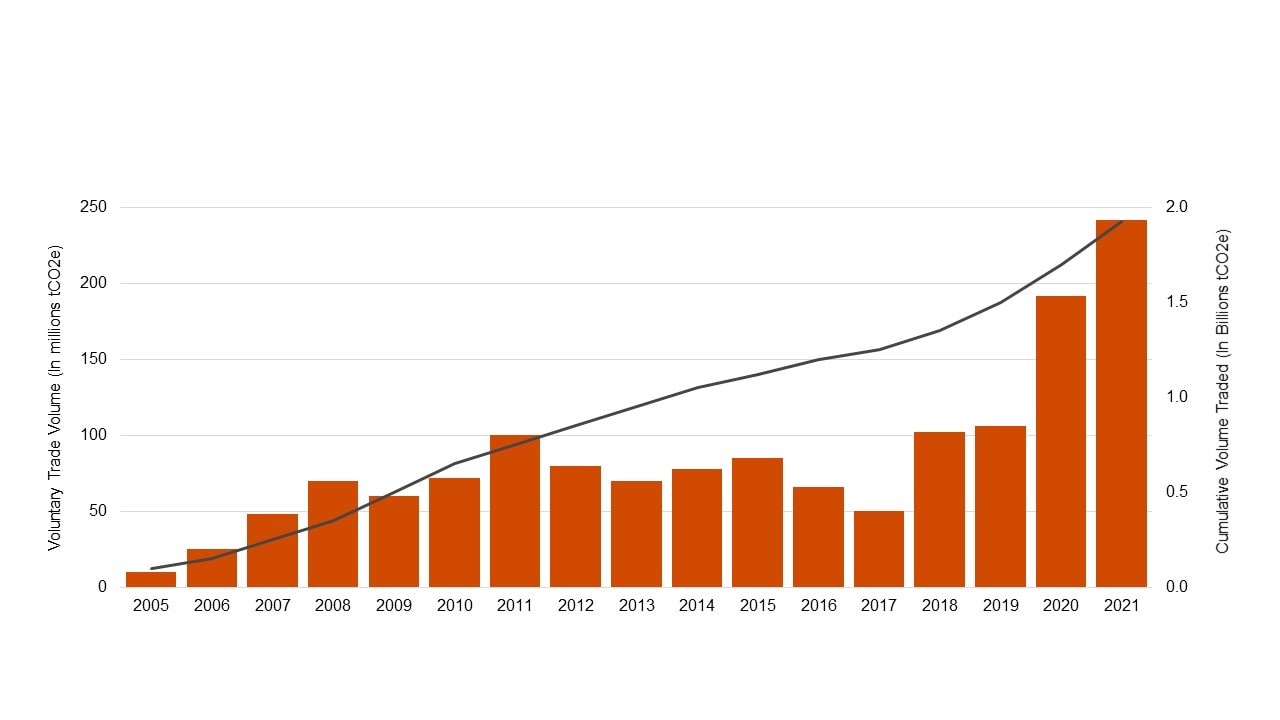

Growth in carbon markets

Globally, voluntary carbon markets have been growing rapidly. The total carbon traded in 2021 was US$851 billion - representing 15,811 Mt of CO2, of which approximately US$2 billion were voluntary carbon credits. The voluntary carbon markets have traded over 239 million tonnes of CO2e in the first 8 months of 2021, a ~ 228% growth on 2019 full year figures.

VCM Carbon Trade Prices & Volumes by Year, pre 2005 to 31 August 2021

Comparing these voluntary carbon markets to the global oil market, which traded at approximately US$10 billion a day in 2022. These figures imply not only that the market has plenty of room to continue growing, but also that growth is essential given fossil fuels are likely to remain part of the transition energy mix, and their associated emissions will have to be addressed.

The US Securities and Exchange Commission is reviewing how to treat carbon credits (and, to a degree, allowances) with current thinking indicating that carbon credits are financial instruments that are traded in the same way as commodities. However, as there are no physical commodities underpinning them, they act more like financial derivatives.

As carbon markets grow, they will seek increasing scale to improve their liquidity and fungibility across an interconnected series of exchanges. This increases the risk that the cornerstone of these markets will be eroded. And what is this basic foundation? Quite simply: trust. Trust in the quality of carbon credits from both the supply and demand side.

The central concept behind carbon credits and their function, is that they can effectively address emissions of an organisation via reduction/abatement, offsetting or removal. However, the question that arises is ‘How can we trust that it actually does address emissions?’ or ‘What is the level of confidence that the credit, which lacks physical tangibility, fulfills its fundamental purpose?’ The measurement of the quality of a credit, and the trust in it, can be somewhat subjective, but it must abide by the following principles: additionality, exclusivity, overestimation and permanence.

Australia’s evolution

In Australia, our maturing carbon market will be exposed to demands and stresses as it grows and becomes more sophisticated. These stresses will be further compounded as the Australian market becomes more globally connected. Recent activity includes:

- Proposed reforms to the National Greenhouse and Energy Reporting scheme’s Safeguard Mechanism, which requires Australia’s largest greenhouse gas emitters to keep their net emissions below a baseline that is in line with Australia’s climate targets;

- The Chubb Review, an independent review of Australian Carbon Credit Units (ACCUs), which concluded that the scheme is essentially sound but that there is room for improvement.

These developments, along with international growth, emerging fungibility and increasing liquidity, will make Australia a valuable player in the global carbon challenge. We may currently be a very small part of the equation – and some of the rules will be set by others – but we can make a huge contribution if we position ourselves correctly. This is the time to get involved.

The impact of quality

What is the value of carbon credits? This is a hot and often-debated topic. In Australia, the recent Chubb Review confirmed that ACCUs are of high quality but noted there is still room for improvement. This is likely to be true for all elements of the carbon markets ecosystem for several years, if not decades.

Perhaps a better question is: How should the race for high-quality credits influence the growth and scaling of the carbon markets?

An immediate response might be that the quality discussed earlier should always come first. However, increased liquidity and fungibility lead to better connectivity across carbon exchanges, which helps market participants through improved price discovery, the emergence of a forward curve for carbon, and ultimately an improved environment within which to manage risk.

With this in mind, the fundamental concept that needs to be considered is, what is the minimum level of quality we can accept? It cannot be too high, or we will risk strangling any proactive involvement in the production of credits, whereas conversely, accepting credits of low quality would flood the market and begin a "race to the bottom" that will ultimately defeat the ideological purpose of having credits at all.

One fact we can rely on however, is that it is impossible to have both an infinite supply of credits, and a perfect quality benchmark. Rather, a threshold needs to be determined that allows a reasonable flow of credits into the market, and still provides legitimate progression to net zero.

Ultimately, both quality and scale may be needed to allow a useful economic value – one that is underpinned by capital market integrity – to be assigned to carbon.

As carbon markets mature and grow, traditional value and risk management tools will become available to the significant number of players involved. The volatility that engages the traders so actively should become more predictable and aligned to the true value and price required for carbon to head towards the best outcome that our global community can achieve.

Pricing carbon

Assuming a trusted and functional connected network of carbon marketplaces, or at least one that is heading that way, we can think about what a carbon price could – and should – look like. Unfortunately, the complexity does not end at creating the marketplace. Like many commodities, carbon is not necessarily comparable across different credits (or allowances).

Efforts to standardise assurance methodologies and strip out, or independently price, the value of associated components (including various assurance methodologies such as the UN Sustainable Development Goals included in the Gold Standard assurance methodology) are progressing. Both single and basket price markers appear to be emerging as a better indicator of the market’s view of the value of the carbon component of a credit.

How credits are being generated also appears to be driving their associated and perceived value. The Australian spot price favours certain methodologies via higher prices and attaches a premium to the level and type of co-benefits associated with a credit’s creation. We have seen prices for abatement activities closely aligned to internal carbon pricing cover a broad price range, which also can vary dramatically by sector.

Prices for credits vary too, but these tend to also rely on a number of factors including the type, standard certification, Co-Benefits/SDGs, vintage, and geography. A discount is often applied to older credits and projects of perceived lower quality.

Source: S&P Global Commodity Insights

One newly emerging price marker is the small but increasing number of transactions in the carbon removals market. These have been priced at a significant premium to both the higher end of internal carbon prices being set by companies and the US$90–130 per t CO2e price that is required for the 1.5°C pathway in the Paris Agreement.

Sources: Trading Economics, Reuters, AFR

With the proposed Safeguard Mechanism potentially leading to higher market prices (which would be capped by the Clean Energy Regulator at A$75 per t CO2e with an annual inflator for now), and increasing confidence in the assurance and accreditation of carbon credits, a supply response will be triggered. We are currently seeing this in Australia, following the Chubb Report and Safeguard Mechanism announcements.

The proposed Safeguard Mechanism amendment to remove the baseline headroom from the 215 participants has also triggered a demand response for the window out to 2030 (and most likely beyond). However, these supply–demand dynamics are not new. Domestically, we have the benefit of hindsight from our observations of the evolution of the more mature global exchanges. These lessons can, and indeed have been incorporated into the proposed design, such as multi-phase banking, levels of flexibility in monitoring periods and extended SMC generation periods which aim to incentivise continual emissions reduction.

If we accept that global carbon exchanges will become interconnected, and carbon exchange rates clarified and agreed, the scheduled provision to review the use of international credits for qualification would be a smart move. However, this would expose the Australian domestic carbon market to the global one, which, as we have seen recently with other commodities (e.g. gas), carries its own challenges.

One final consideration. As much as we look to protect our emissions-intensive trade-exposed companies through measures such as the Carbon Border Adjustment Mechanism (CBAM), there is also a risk of high-quality projects in Australia monetising their carbon credits overseas. This would lead to the market not performing the role it was established to do for Australia. Instead, it would leak carbon overseas, helping to contribute to other countries' Nationally Defined Contributions (NDCs) but potentially solving the Global problem in a more efficient way.

Generating Value

Assuming that the carbon markets are functioning efficiently, and the carbon price is accurate, the next challenge is to generate value. There are many different strategies for monetising carbon.

At the simplest level, on the supply side, credits can be generated by reducing/abating, offsetting and/or removing carbon. On the demand side, the choice or obligation to reduce emissions triggers a liability and the need to acquire such credits.

What happens when we implement the Safeguard Mechanism?

How will our entry into the global marketplace impact supply and demand?

Internationally the underlying marketplace of supply and demand is growing, connecting and becoming more sophisticated, leading to the traditional activities of trading and opportunistic investment will emerge.

Australia’s carbon market is maturing and evolving rapidly. Coupled with our broad and expanding renewable energy portfolio, perceived high-quality credits and an evolving domestic market, this sets the stage for significant opportunities at scale to generate value from carbon and accelerate our progress towards decarbonisation.

This might seem too good to be true. The catch is that Australia needs to access this value in a rapidly changing global carbon ecosystem. And we are not the only country looking to capitalise on the evolving dynamics of carbon markets.

Risks – such as an erosion in trust of ACCUs, missteps in the Safeguard Mechanism reforms, the implementation of Articles 6 and 6.2 of the Paris Agreement (when they are finalised) and even uncertainty around how local credit generation is incentivised to remain onshore and contribute to Australia’s nationally determined contributions rather than being traded offshore – must be actively tracked and managed, as the complexity and sophistication of those risks are also evolving at a rapid rate.

Opportunities in Australia

The carbon markets in Australia present a huge opportunity for domestic players and overseas investors. There are four clear opportunities:

- addressing existential threats

- capitalising on advantaged positions

- monetising productivity opportunities

- creating pathways to manage risk.

Addressing existential threats

Opportunities exist where companies must reduce their reliance on carbon in order to survive. Often this takes them from an emissions-intensive position to a carbon-neutral or even carbon-negative one. These companies are often looking to share the risk and may need additional capital. These can be high-value, high-risk plays for an overseas player, but can be used as proof-of-concept to create a world-leading transition play that can be rolled out globally.

Capitalising on advantaged positions

These opportunities can arise when an established, well-known and understood player wants to actively decarbonise to maintain its market leading position, or when a niche, rapidly scaling energy transition player wants to capture excess returns while it is in an advantaged position. While the former is a more traditional player in the carbon markets, looking for opportunities to comply with regulation and monetise carbon on a case-by-case basis, the latter can be a target for capital investment to help it accelerate its scaling and build a robust position on the supply side of the carbon credit ledger.

Monetising productivity opportunities

Carbon emissions and carbon intensity have been a focus of continuous improvement programs for many years in Australia and internationally. This has often been driven by a loosely linked ESG strategy and incentivised by traditional economics and / or an internal carbon price. The increasing confidence in and integrity of the carbon markets has put internal carbon prices back in the spotlight. Opportunities exist to increase internal carbon pricing and drive a broader suite of decarbonisation opportunities, especially if they can connect to the hybrid ACCU market.

Creating pathways to manage risk

Hard-to-abate sectors, such as concrete and steel manufacturing, receive a significant amount of attention in the media because of their volume weighting and abatement complexity. Barring a bold opportunity to evolve a hard-to-abate sector, opportunities will exist to leverage the carbon markets to comply with emissions obligations and to source capital for innovation in technical solutions. Connecting global carbon exchanges to ensure the lowest-cost abatement and removal opportunities are being captured will provide much-needed time for these sectors to transition in an orderly fashion.

In addition to the participants in the market, there are also opportunities where value creation by companies developing the ancillary services required by the markets and their participants, such as ranging, baselining, assurance, certification and carbon isotope tracking.

Hope for the future

The solutions to decarbonisation are far from simple. They require collaboration and the ability to work in ways that are very unfamiliar to most businesses. Carbon markets can play a pivotal role in valuing carbon, facilitating reallocation of capital to fund decarbonisation activities, and sharing the carbon price risk.

There will be upsets along the way, but hopefully the markets will be robust enough to absorb them without losing momentum. Decarbonisation is within our reach and opportunities exist to participate in and benefit from domestic and global carbon markets now.