{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

It’s impossible to state definitively where the world stands when it comes to the pandemic and its effects on business. The findings from this year’s 25th Annual Global CEO Survey were fielded in October and November of 2021. At the time, 77 percent of the 4,446 participating CEOs said they expected global economic growth to improve.

Of course since then, in a mere couple of months, the world has been shaken by the Omicron variant’s emergence and domination. There is no question that the course of the pandemic remains uncharted, and whether or not the world can return to normality anytime soon undecided. But at least at the end of last year, global GDP was predicted to grow and CEOs remained optimistic when it came to economic resilience.1

CEOs are not only positive about the world’s prospects for growth, they’re at their highest level of optimism since the CEO Survey began asking the economic potential question back in 2012. That being said, there are discrepancies between countries reflecting differing realities and perspectives on the future.

CEOs in Brazil, China, Germany, and the United States report feeling less optimistic than they were a year ago, fearing growth rates are poised to increase, whereas those in Australia, India, Japan, and the UK are more optimistic than they were last January.

Such differences may simply reflect where CEOs see themselves in the economic cycle. China and the US, for example, rebounded ahead of the rest of the world and are now experiencing growing pains in the form of inflation, real estate bubbles, and supply chain disruptions. Both countries are also confronting labour shortages. In China, shifting demographics and structural unemployment are creating a growing gap;2 in the US, headlines about ‘the great resignation’ and early retirement predominate.3

In Australia, the economic impact of the first waves of the pandemic was less than feared given strict border closures and strong public health measures. Going into 2022, however, Omicron has already proven challenging for supply chains, healthcare systems and labour.

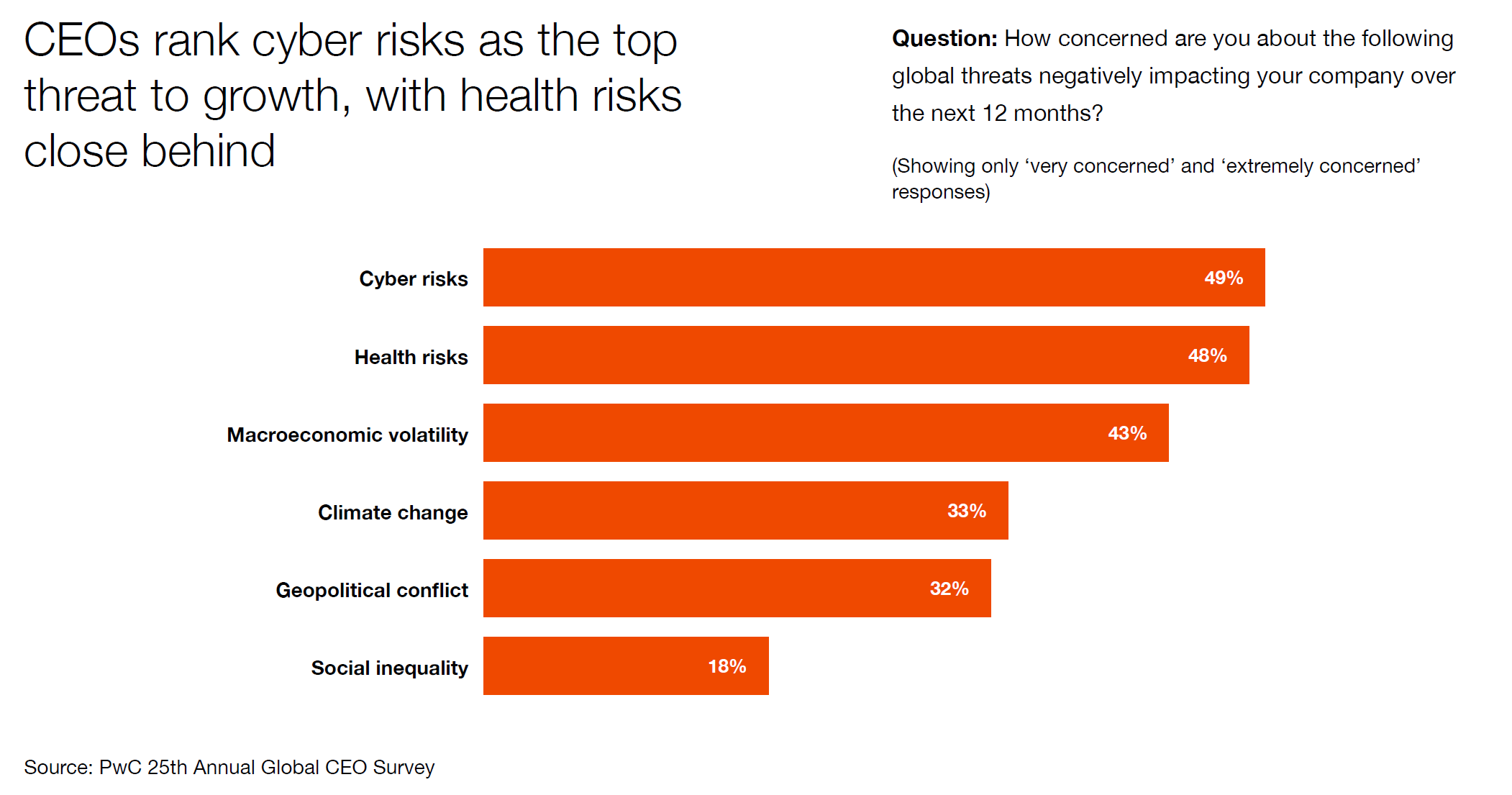

Surprisingly, considering the impact of COVID-19 on the last two years, the pandemic is not the threat that CEOs are most worried about when it comes to their businesses. While it lurks nearby, selected under ‘health risks’ by 48 percent of global CEOs as a threat to business, it is in fact cyber risks, at 49 percent, that troubles top executives more.

An ongoing concern, a significantly higher proportion of Australian CEOs are worried compared to their global counterparts, with 71 percent citing that they are very or extremely concerned – 22 percentage points higher than the global average. In comparison, health risks such as the pandemic, came a distant second at 55 percent very or extremely concerned for Australian chief executives.

This alarm is perhaps understandable, with ongoing and sustained attempts by state-based cyber-actors targeting government institutions and businesses, but when asked what was influencing their cyber security strategies, Australian CEOs pointed to the increasing complexity of cyber threats (82 percent) and cyber data/privacy regulations (69 percent). At much higher levels than last year, vulnerabilities in supply chains and those of their business partners (69 percent versus 44 percent) and a shortage of talent (41 percent, up from 23 percent) were of concern.

Indeed, in PwC Australia’s Global Digital Trust Insights 2022, 66 percent of respondents predicted an increase in cybercrime, and 70 percent said they expected nation-state attacks to grow. While interconnectivity topped the list of vulnerabilities, respondents were broad ranging in the form of attack they expected, with software supply chain breaches (72 percent), state-sponsored attacks on critical infrastructure (69 percent) and ransomware (68 percent) as the most likely predicted to increase.

Interestingly, manufacturing (40 percent) and consumer (39 percent) CEOs globally displayed lower levels of concern about cyber, despite those sectors’ high volume of cyber attacks.4 Coming in a close third on the threat list is global CEOs’ concern about macroeconomic volatility, including fluctuations in GDP and unemployment, and inflation.

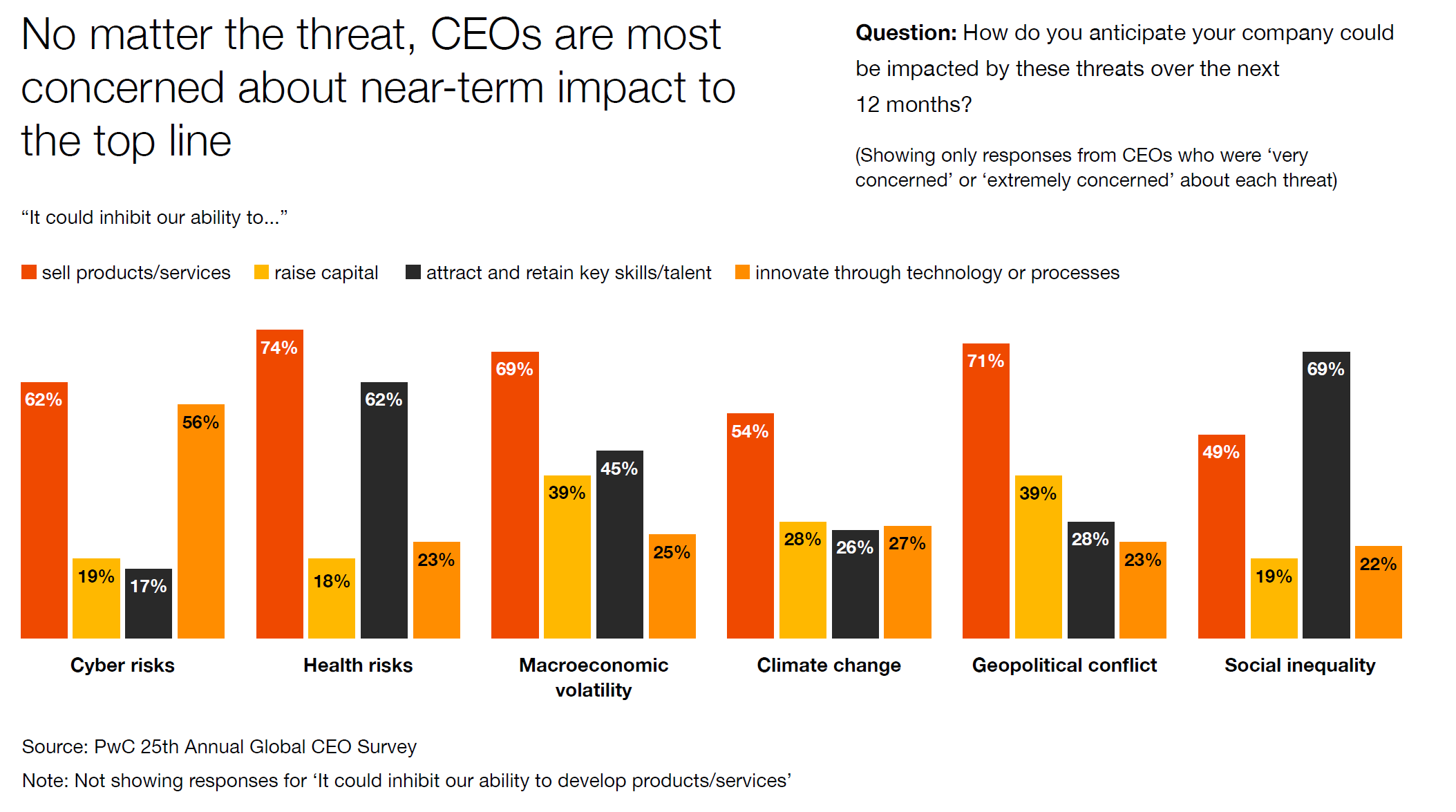

Global CEOs expanded upon what they thought each threat could do to inhibit their ability to achieve business outcomes over the next 12 months. With the exception of social inequality, global CEOs were most concerned about the potential of each threat to disrupt revenue.

Australian CEOs were generally more positive about growth than their counterparts, especially when it came to the country and organisational prospects. Eighty-eight percent of Australian CEOs believe there will be positive growth domestically in the next 12 months, and while slightly more than half of the surveyed global CEOs report high levels of confidence about their own prospects for revenue growth over the next 12 months – a much larger 67 percent of Australian chief executives report being very to extremely confident in the ability of their own businesses to track upwards.

Globally, the most growth-optimistic CEOs are of private equity (67 percent) and technology companies (64 percent). Both sectors continue to benefit from large inflows of capital, thanks to the favourable financial conditions prevailing in most advanced economies. Among the CEOs on the other end of the spectrum are those in the automotive (46 percent) and hospitality and leisure sectors (44 percent), grappling with semiconductor shortages and the lingering effects of the pandemic on travel, respectively.5 It remains to be seen whether the pandemic trajectory will shift and present new constraints on some industries.

Innovation, of course, fuels growth and with funds flowing into startups, opportunities for larger companies should come from the generation of economic activity. While new capabilities may need to be attained, opportunities will likely come for larger established companies in areas such as the platformisation of consumer financial services, the electric vehicle ecosystem and stored energy, the creation and expansion of the metaverse, the ongoing convergence of mobility and digital commerce, and the virtual evolution of health and wellness. It is worth noting, however, that this year’s survey also found that CEOs are worried that cyber risks could inhibit their innovation efforts.

This year, the PwC Annual Global CEO Survey turns 25. In 1997, the first survey found that change was in the air, driven by information technology. Since then, CEOs have informed the survey on a variety of pivotal societal moments. The dot-com bubble in 1998 hinted at the future of e-commerce and the true impact of the internet to daily life. Corporate scandal brought enterprise risk management and corporate governance to the fore in 2003, followed by the global financial crisis in 2008.

When the survey began, no one could have predicted the turbulence and uncertainty that a global pandemic like COVID-19 would bring 25 years later, nor the magnitude and immediacy of addressing climate change – another key focus of this year’s findings. As the report concludes, “the need for decisive action has perhaps never been as strong. Business as usual isn’t mitigating the climate crisis, or bridging the socioeconomic divide. The results of the CEO Survey lay these truths bare—and underscore the need for bold leadership to unite us as global citizens and problem solvers.”

View the findings from the full PwC Annual Global CEO Survey or explore Australia-specific insights.

References